The illusion of stability

How a fragile ceasefire is exposing the world's hidden instability

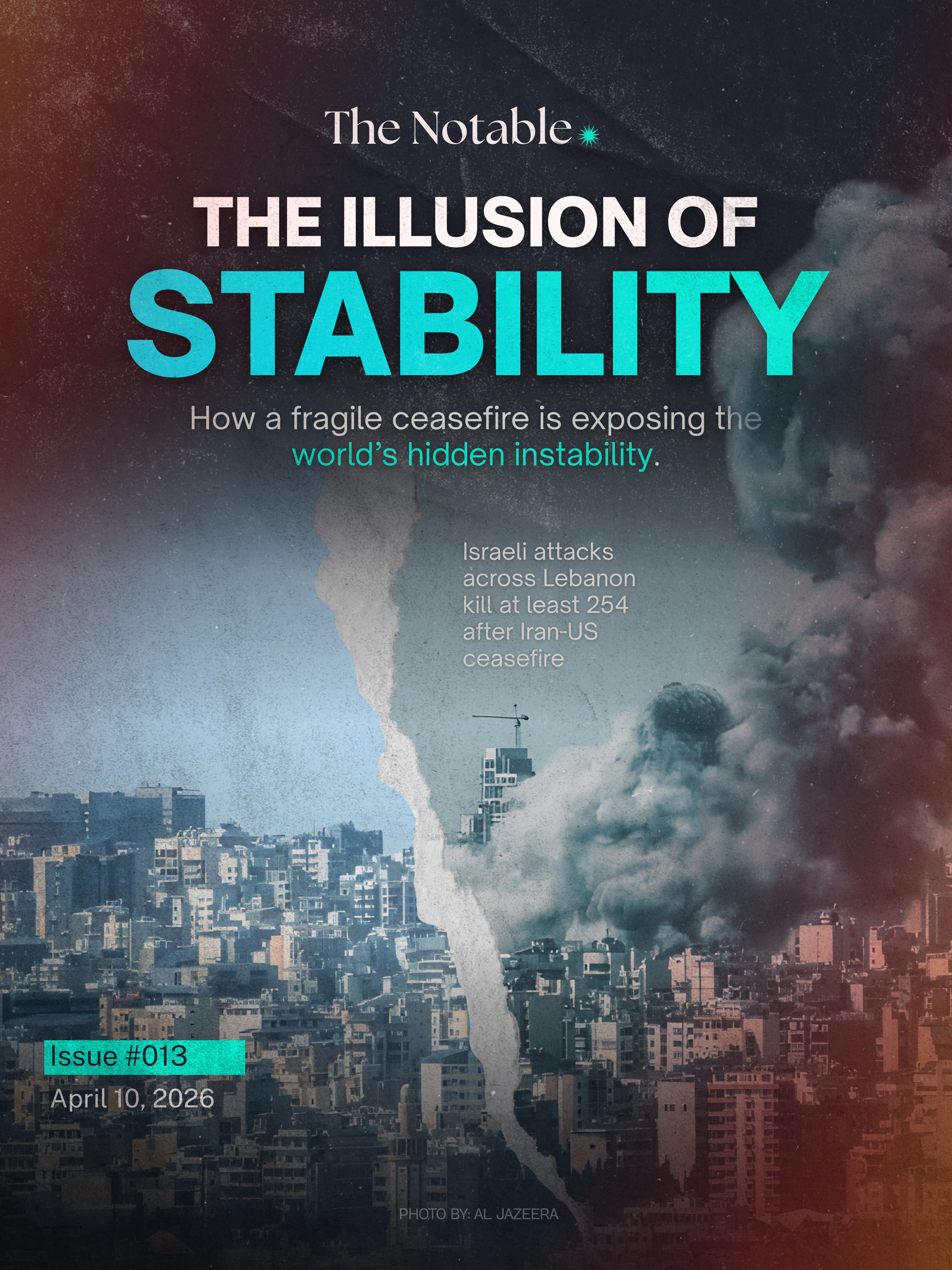

A few hours after markets exhaled, the airspace over southern Lebanon did not.

Fighter jets crossed quietly. Targets were hit. The logic of the battlefield continued, even as the language of diplomacy suggested something else.

At nearly the same moment, oil traders were doing the opposite. Prices, which had surged days earlier, began to ease. Headlines shifted tone. The word “ceasefire” entered the system, and with it, a familiar assumption that escalation had been contained.

From a distance, the sequence looked orderly. Tensions rise, markets react, leaders intervene, stability returns.

But the sequence was misleading.

Because nothing about the underlying system had actually stabilized.

In early April, the confrontation involving Iran forced global markets to confront something they have long understood but rarely priced properly. The modern economy runs through narrow channels, and those channels do not need to break to create disruption. They only need to appear vulnerable.

The Strait of Hormuz is one of those channels. Roughly a fifth of the world’s oil moves through it. When tensions escalated, prices surged almost immediately. Not because supply had collapsed, but because the risk of collapse had become credible.

That distinction matters.

The system did not wait for disruption. It reacted to the possibility of it.

Within days, inflation expectations began to shift again. Central banks, which had spent months trying to guide economies back toward price stability, were forced to reconsider how quickly that stability could unravel. The chain reaction was familiar but increasingly compressed. Geopolitical tension feeds energy markets. Energy markets feed inflation. Inflation constrains policy.

The speed is what has changed.

Then came the ceasefire.

Prices softened. Markets steadied. The narrative adjusted almost instantly. What had been framed as escalation was now described as containment. The system appeared to have absorbed the shock and returned to balance.

But this is not a story about balance.

It is a story about how balance is inferred, often too quickly, from surface signals.

The ceasefire did not resolve the underlying tensions. It reduced their visibility. And in doing so, it triggered a reflex. Markets and institutions reverted to a working assumption that the system had stabilized.

But stability, in this context, is being misread.

What looks like calm is often just a reduction in noise.

The continued strikes by Israel inside Lebanon expose this gap between perception and reality.

Formally, a ceasefire signals de-escalation. In practice, it often marks a shift in how pressure is applied. Direct confrontation may ease, while targeted operations continue in parallel. Strategic objectives remain unchanged. They are simply pursued with different intensity and visibility.

For Israel, halting entirely would introduce its own risks. It would allow Hezbollah to regroup and reinforce its position. Continuing limited strikes preserves deterrence and signals that a ceasefire does not imply strategic pause.

This is not an exception to the system.

It is how the system now operates.

Conflict no longer moves cleanly between war and peace. It moves between higher and lower intensity. The activity does not stop. It redistributes.

This matters because the global economy is not built to interpret nuance. It is built to interpret signals.

And increasingly, those signals are being misinterpreted.

When oil prices fall, the system reads relief. When headlines mention ceasefire, the system reads de-escalation. But these signals are partial. They reflect visible changes, not underlying conditions.

The deeper condition has not improved.

It has only become less obvious.

What makes this moment more significant than previous episodes is not the existence of risk, but the system’s sensitivity to it.

In earlier decades, major economic disruption typically required sustained physical shocks. The 1973 oil crisis, driven by coordinated production cuts from OPEC, reshaped global inflation and growth because supply was materially constrained over time.

Today, the threshold is lower.

A credible threat, even if short-lived, can move markets, alter expectations, and influence policy decisions. The reaction function has accelerated. Signals that once would have been absorbed are now amplified.

Volatility has become anticipatory.

This shift extends beyond energy markets.

Financial systems now transmit geopolitical risk with almost no delay. Capital moves quickly toward perceived safety and just as quickly back toward risk when conditions appear to improve. These movements are not always anchored in long-term fundamentals. They are responses to rapidly changing expectations.

The result is a system that oscillates.

Not between stability and crisis, but between different interpretations of risk.

Central banks are operating within this oscillation.

Institutions like the European Central Bank and the Federal Reserve are tasked with managing inflation and economic stability, but their tools are designed primarily for domestic conditions. Interest rates can influence demand. They cannot stabilize a shipping route or prevent a geopolitical escalation.

This creates a structural constraint.

Policy can respond to the effects of instability. It cannot prevent the causes.

The International Monetary Fund has begun to signal this more explicitly. Its managing director, Kristalina Georgieva, has warned that geopolitical shocks of this kind may leave lasting marks on the global economy. The implication is not just that growth may slow, but that volatility itself may become embedded.

Stability, in other words, may no longer be the default state.

There is another layer to this shift, one that is less visible but equally important.

The global system has memory.

The supply chain disruptions of recent years have changed how companies respond to early signs of risk. Businesses that once optimized for efficiency are now more likely to hedge against uncertainty. They reroute shipments earlier, build larger inventories, and adjust sourcing strategies at the first indication of disruption.

These actions are rational at the firm level.

Collectively, they amplify system-wide reactions.

A signal that might once have produced a delayed response now triggers immediate adjustments across multiple sectors. The system becomes more responsive, but also more volatile.

At the same time, the world is attempting to transition its energy base.

Renewable energy is expanding, but the global economy remains heavily dependent on fossil fuels, particularly for transportation and industrial activity. This creates a structural contradiction. The system is trying to evolve away from the very resources that continue to anchor its stability.

Until that transition is complete, chokepoints like the Strait of Hormuz will retain disproportionate importance.

The system is, in effect, moving forward while still anchored to its most fragile components.

Taken together, these dynamics point to a broader shift.

The global economy is no longer defined primarily by its capacity for efficiency. It is increasingly defined by its exposure to disruption.

Efficiency has not disappeared. It still drives production, trade, and growth. But it now coexists with a level of fragility that is harder to manage and easier to trigger.

The result is not constant instability.

It is intermittent stability.

Periods where the system appears to function smoothly, interrupted by moments where its underlying vulnerabilities become visible again.

This is why the events surrounding the ceasefire are easy to misread.

They fit a familiar pattern. Tension rises, then falls. Markets react, then recover. The narrative resets.

But the pattern itself has changed.

The recovery is faster, but so is the disruption. The calm feels real, but it is often shallow.

And the underlying conditions remain unresolved.

The jets over Lebanon did not contradict the ceasefire.

They clarified it.

Because they revealed that what appears as resolution is often just a shift in visibility. The system continues to operate beneath the surface, driven by incentives that do not pause simply because the language of diplomacy changes.

The same is true for markets, for policy, and for the global economy itself.

Nothing fundamental has been stabilized.

The signals have simply become quieter.

And for now, that is enough to be mistaken for calm.